The Campbell’s Company (NYSE: CPB) reported its Q3 2026 earnings report on June 8. The results were mixed and included a surprising earnings beat. But the topline showed that the company still faces competitive pressure, even as more consumers eat at home.

The culprit is inflation. In 2020 through 2024, Campbell’s benefited from the pantry-stocking trend. But it’s been a different story in the past 18 months, as the company has faced tariff pressures that put it in a tight spot. In “normal” times, Campbell’s could pass along its costs, but that’s not possible with a lower-income consumer who’s actively seeking value in house brands.

However, CPB stock is down 37% over the last year and pays a dividend yield of over 7%. That could make a tempting case for buying CPB as a deep value play. But before you do, you should look at the company with clear eyes. The company faces real pressure, as do its core consumers. But if you can get past some near-term ugliness, the stock may be a strong compounder that could be comfort food for your portfolio.

A Tale of Two Companies

Campbell’s Q3 results tell a tale of two companies living inside the same ticker. On the surface, GAAP net earnings of $124 million looked considerably better than the $66 million reported in Q3 FY25. But that comparison is misleading — last year’s GAAP figure was hammered by $150 million in impairment charges. Strip those out, and the adjusted picture tells a different story: adjusted EPS fell 32% year-over-year to $0.50, while adjusted EBIT dropped 24% to $274 million on a margin that compressed from 14.6% to 11.6%.

Net sales declined 4% to $2.37 billion, driven by a 5-point volume/mix headwind that pricing could only partially offset. Tariffs were a meaningful contributor, accounting for 310 basis points of the 630-basis-point gross inflation headwind — equivalent to $0.19 gross per share, or $0.07 net after mitigation. The company reaffirmed full-year guidance calling for organic net sales of (2)% to (1)% and adjusted EPS of $2.15 to $2.25.

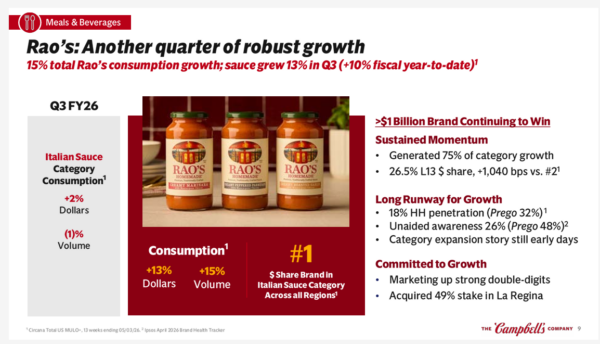

The one genuine bright spot is Rao’s, which posted 13% dollar consumption growth in sauce during the quarter and generated 75% of total Italian sauce category growth. With only 18% household penetration versus Prego’s 32%, and unaided brand awareness at 26% versus Prego’s 48%, the runway remains long. Campbell’s is investing behind it (double-digit marketing spend), and the recent 49% stake acquisition in La Regina adds an authentic Italian sourcing angle that could further differentiate the brand.

The same can’t be said for the Snacks segment. Dollar consumption fell 5%, and operating margin collapsed from 14.3% to 10.1%. The Pepperidge Farm fresh bakery network is stabilizing but not yet recovered, and the salty snacks portfolio (e.g., Cape Cod, Snyder’s, Late July) needs a portfolio simplification and a price-pack architecture overhaul, both of which management acknowledges will take time. Goldfish showed sequential improvement and maintained dollar share, offering a sliver of optimism.

The Psychology of Soup

Lower- and middle-income consumers are feeling the pinch of high inflation. That doesn’t just benefit discount retailers like Dollar General (NYSE: DG), it also gives private-label brands a bump. Ever since the generic trend started in the 1970s, house brands (i.e., private label) have become the low-cost option for consumers. That hits a company like Campbell’s hard because it’s hard to create a value proposition beyond price for products like canned soup or broth.

Before you dismiss this as speculation, consider the reality behind these consumer perceptions. A First Insight study in January 2025 cited that 71% of consumers believed they could recognize a private-label brand when shopping. However, 72% were actually unable to tell the difference when shown side-by-side images of store-brand and national-brand products. That’s a hit to a company like Campbell’s that relies on a brand premium as part of its growth case.

And the problem becomes entrenched once consumers switch to a private label brand. A 2026 survey of 1,010 U.S. adults found that 60% had dropped a brand they were loyal to because of rising prices, with grocery being the most affected segment at 76%. That far outpaced personal care, household goods, and clothing. Critically, 69% of respondents felt store brand products were “just as good” as name brands.

What makes this particularly damaging for Campbell’s is that the switching behavior tends to be permanent. Research shows that consumers who purchase private label products for 18 to 24 months form new shopping habits that persist well beyond the economic conditions that triggered the switch. Nearly half of consumers who switched said they had no intention of returning to the national brand. Private-label soup and snacks have already gained an estimated 200 basis points of market share at Campbell’s expense over the last 18 months as Walmart (NASDAQ: WMT) and Kroger (NYSE: KR) aggressively expand their house-label portfolios.

But not all of Campbell’s portfolio is equally exposed to this threat. The private-label risk is concentrated in commodity-adjacent categories (e.g., condensed soups, RTS soups), where products are largely undifferentiated and switching costs are near zero. Rao’s operates in an entirely different psychological register. It’s a premium, identity-linked brand with genuine taste differentiation.

The Tepid Bull Case

After a dismal 12-month period that has seen the price drop over 37%, CPB stock appears to have found a bottom. The stock is down after the earnings report, but volume is light. That’s not insignificant, with over 20% short interest in the stock.

The bears have made their point, but can buyers mount a rally? Institutions haven’t given up on Campbell’s, but the stock doesn’t show much upside at the moment. It’s trading about 5% below its consensus price target of around $22.80.

That aside, despite the eating-at-home trend remaining in place, CPB is not the same stock it was just two years ago. In fact, the stock is trading right about where it was in 2011. That’s a big haircut for buy-and-hold investors to swallow.

But Campbell’s does offer an attractive dividend. Investors shouldn’t be seduced by the yield of over 7%. That’s largely a function of the stock price decline. The key for investors is that the dividend appears to be stable. The company hasn’t cut the dividend since 2001.

Campbell’s also looks tasty on valuation. At around 9x forward earnings, it’s trading at a discount to its historic average and to the consumer staples sector.

Is CPB Stock Worth the Risk?

The real question for investors is whether Rao’s can grow fast enough to offset secular erosion in legacy soup. The brand generated 75% of the Italian sauce category growth this quarter while sitting at just 18% household penetration. If management can close even half the awareness gap with Prego and extend the brand into adjacent categories — soups, frozen meals, foodservice — the long-term earnings trajectory looks very different from what the current stock price implies.

That said, CPB is not a stock for investors who need near-term catalysts. But for investors with a 3-to-5-year horizon who can stomach continued volatility, the combination of a deeply discounted valuation, a durable dividend, and a genuine premium brand in Rao’s with significant room to grow makes Campbell’s a cautious buy. The company’s own guidance points toward an improving trajectory into fiscal 2027. If management executes, the current price may look like an opportunity in hindsight.