Skeptics warned that retail money would become exit liquidity the moment Space Exploration Technologies Corp (NASDAQ: SPCX) hit the public market. That prophecy has now come to pass.

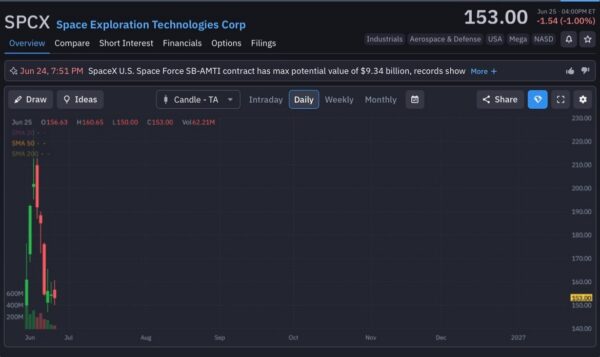

SpaceX priced its IPO at $135, opened at $150, and surged to an intraday high of $225.64 on June 16, briefly pushing its market capitalization above $2 trillion and making Elon Musk the world’s first paper trillionaire. Then gravity took over.

The stock has already fallen more than 30% from that high in roughly a week. Today, it trades around $153, almost exactly where it opened on day one and has almost completely retraced the euphoric rally that followed the listing. The heaviest selling arrived alongside massive volume, showing this wasn’t retail investors taking a few profits but sustained distribution as enthusiasm gave way to valuation. Momentum still points lower and the chart could continue favoring the bears until it hits what I call its true market price of $50-$60. Let me explain.

Trapped In The Float

Only about 4-5% of SpaceX’s shares actually trade. The remaining 95% remain locked behind staggered lock-up agreements stretching from late July through June 2027. Selling windows don’t begin opening until late July, the standard lock-up doesn’t expire until December, and Musk himself can’t sell until June 2027.

A market that thin doesn’t discover a fair price. It manufactures one. No wonder a handful of buy orders was enough to launch SpaceX into the stratosphere during its first week because almost nobody could sell into the demand. The same mechanism now works in reverse. Relatively small amounts of selling produce violent price swings because the market still lacks the liquidity needed to absorb them.

Retail investors believed they were buying into conviction, and I can’t blame them especially if they missed out on Tesla’s ginormous gains, but sadly, the story isn’t the same anymore, because what they actually bought was a stock with almost no natural liquidity, leaving price movements far more sensitive than the underlying business ever was.

Strip Away The Hype And The Math Drops To The $50-$60 Range

Strip away reusable rockets, Mars colonies, and Elon Musk’s aura for a moment, and the valuation starts looking much harder to defend.

SpaceX’s actual, provable revenue comes overwhelmingly from Starlink, which generates roughly $20 billion annually once you set aside the company’s aggressive accounting around satellite replacement costs. That makes SpaceX, in practical terms, a telecom company wearing a space-exploration costume. Give that telecom business a generous 10x price-to-earnings multiple – already rich for the sector – and you land on a roughly $200 billion valuation. That’s about 90% below where this stock peaked, and still well below where it trades today.

Even assigning Starlink a generous valuation produces numbers nowhere near where the market currently prices the company. A business generating roughly $20 billion in annual revenue doesn’t suddenly justify a valuation approaching $2 trillion because investors expect it to conquer Mars one day.

Now take the current price and divide it by roughly ten, and you land in the same $50-60 range I keep coming back to as the level where this stock actually reflects what the business produces, instead of what Elon Musk’s name produces.

Everything else supporting the bull case, from Mars colonies and space-based data centers to asteroid mining, belongs to a future that may arrive decades from now. None of it generates cash flow investors can value today. Starship and the launch business may eventually become enormously profitable. Today’s valuation already assumes much of that success before it has happened.

But great companies don’t automatically become great stocks. Price still matters. And speaking of price, short interest in SpaceX jumped from roughly 8% to 13% in a single trading session, a sign that bearish conviction is spreading beyond retail skeptics and into institutional positioning.

At the same time, SpaceX confirmed its first-ever bond issuance. Which is quite telling because a company that recently raised $75 billion in equity ordinarily wouldn’t be expected to return to debt markets almost immediately. Investors naturally begin asking whether the company’s capital requirements remain far larger than the IPO narrative suggested.

The skepticism no longer ends with SpaceX. OpenAI is considering delaying its own IPO until 2027, partly because SpaceX’s listing demonstrated just how quickly enthusiasm can evaporate once valuation becomes the dominant conversation. That’s the real signal. When the next company in line starts rewriting its own timeline because of what just happened to you, nobody is questioning the rocket science anymore. They’re questioning the price.

Where I Stand

Just like I said the last time, it can be unreasonable to bet against Elon. I still stand on it. However, I’m bearish on SpaceX at current levels, and I’ll stay bearish until the stock trades much closer to what the business can actually justify, somewhere around $50-60 per share instead of the $150-225 range retail investors rushed to pay during launch week.

It’s obvious that this isn’t a brief dip on the way back to new highs. But a thinly-traded, hype-priced stock finding its real ceiling for the first time, with 95% of its shares still waiting to hit the market once lock-ups start lifting in late July. And I still believe this lead balloon hasn’t finished falling yet, it’s only catching its breath before the next leg down