Earnings season is being talked about in the past tense. That’s fitting, because one of the stragglers left to report is Nike Inc. (NYSE: NKE). Like earnings season, many investors have taken to talking about Nike in the past tense. There are reasons for that, and it’s a shame.

Nike reports earnings on June 30, and it’s doubtful the company will tell investors anything they want to hear.

But does that merit NKE trading at 2015 levels?

That’s a question that investors will answer. We don’t invest in an efficient market. In better days, NKE stock was worth what investors were willing to pay, which was enough for Nike to split its stock seven times since going public in 1983.

Today, Nike is seeing the other shoe drop. The company is in the middle of a turnaround, but right now, that sounds like a company playing defense. A better strategy might be for the company to go on offense.

I love analyzing and writing about stocks. But before that, I spent a lot of time in marketing, and I believe that Nike has a marketing problem. So, if I were to write an open letter to Nike management, here’s what I’d say:

Please, Nike. Just Do It.

An open letter to the swoosh — from an investor who still wants to believe

Dear Nike,

Let me take you back to a simpler time.

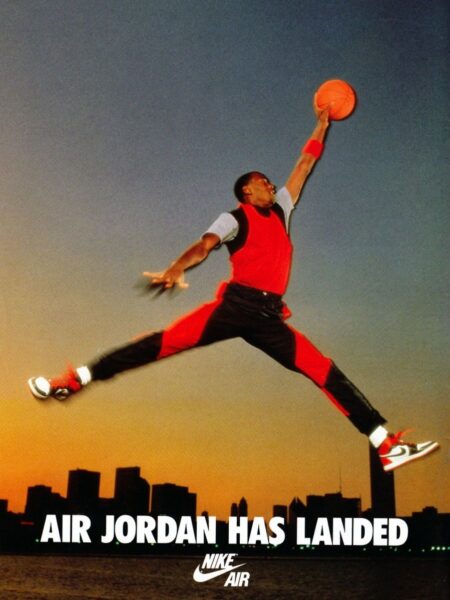

It’s 1992. Michael Jordan is in the air — literally.

He’s palming a basketball with one hand, his tongue out, legs spread like he owns the stratosphere.

The logo below him doesn’t even need a name. You know exactly whose shoe it is.

You know exactly whose company it is. And you know, without question, who runs the athletic footwear world.

That was you, Nike. That was all you.

I’ll be honest — I was a Reebok kid. I liked being the underdog. I liked the rebellion.

But I respected Nike the way you respect a champion you can’t quite beat. You were Coca-Cola (NYSE: KO). Reebok was Pepsi (NASDAQ: PEP). And no matter how good the challenger tasted, the original was still the original.

So what happened?

You Got Lost on the Way to the Trophy Case

Your quarterly earnings report is coming up on June 30. And to be honest, the numbers aren’t going to matter. Investors know it’s going to be a meh print.

Free cash flow has compressed dramatically — down from $3.27 billion in fiscal 2025 to a trailing twelve-month figure around $1 billion today. Gross margins are getting eaten alive by tariffs, down 130 basis points to 40.2% last quarter. Net income fell 35% year-over-year in Q3.

None of those is likely to be much better in the quarter just ended.

Your stock is trading near 2015 levels, around $46, well below its 200-day moving average, which has been pointing south for a year.

And yet, here’s what I’d argue: the market has overcorrected. At roughly 30x earnings, your stock isn’t dramatically expensive by historical standards. You don’t have a broken business. You have a distracted one.

The Reebok lesson should have stuck. There will always be an Adidas (OTCMKTS: ADDDF), an On Running, a Hoka nipping at your heels. You can’t win by trying to be everything. The agile competitor never sleeps. The only antidote is to be so good at what you do best that the challenger never lands a clean hit.

Somewhere along the way, you drifted. You went deep into the equipment. You expanded aggressively into apparel. The sneaker game — the thing that made Nike a religion — got complicated. You chased growth in every direction, and in doing so, you gave the competition room to breathe.

The World Cup Is Your Open Door

Here’s the thing about the 2026 FIFA World Cup happening right now on home soil: Adidas is the official tournament sponsor. They’re everywhere. The branding, the match balls, the pavilions. They bought the headline.

But you outfit Team USA.

And let me tell you something about the American sports fan. We are, almost entirely, World Cup casuals. We’ll watch Team USA play, and we won’t watch much else. There’s a reason most Americans still call it soccer.

That’s not a knock; it’s an opportunity. Because the casual American viewer watching the U.S. national team isn’t already loyal to Adidas. They’re watching American athletes in American colors — and you dress them.

Be the boss. Be the brand that doesn’t apologize. You have done this before. You have made counterprogramming look like leadership.

Run the campaign. Make it loud. Make it feel like 1992 again — hungry, confident, a little dangerous. Don’t let Adidas own the summer while you quietly wait for the noise to die down. This is a moment. Take it.

The Marketing Problem Is Real — But So Is the Fix

The deeper issue is identity. Nike has, almost without realizing it, become a challenger brand. You’re playing defense against On Running and HOKA on performance, against New Balance and Adidas on lifestyle and retro appeal. That’s not a position you play well, and it’s not a position Nike should be in.

The path back is not complicated, even if it requires courage.

Bring Jordan back.

Not the Jordan brand as a sub-label — the man himself. Go nostalgia. Tap into the cultural nostalgia economy that has made everything from vintage jerseys to 1980s movie franchises bankable again. Gen Z and Gen Alpha don’t remember the first Air Jordan era. Show them what they missed. Make them feel like they’re discovering something. You have arguably the greatest marketing asset in the history of sports sitting in North Carolina. Use him.

And on the product side — get back to the shoe. Run the retros. Do the heritage drops. But also create the next Air Max moment. The next Pegasus. The next shoe that a teenager will remember wearing when they were fifteen.

The Hard Stuff: Tariffs and Manufacturing

Let’s be real about the headwinds. Tariffs are cutting into margins with no near-term relief. Nearly all of Nike’s production is outsourced to contract manufacturers across more than 30 countries, and reshoring — even partially — would take years and cost billions. Management knows this. Investors know this.

What the June 30 earnings call needs to deliver is not a miracle. It’s a credible plan. Show investors that the restructuring is working. Show that inventory discipline is holding — it is, with inventories down 1% year-over-year. Show that North America is stabilizing — wholesale revenue was up 5% last quarter. And show that the marketing machine is coming back online in time to capture the World Cup moment.

Cash and short-term investments still total $8.1 billion. That’s not a company in crisis. That’s a company with choices. Choose wisely.

Back to the Locker Room

So here it is, Nike. The speech before the game.

You are not a startup figuring out who you are. You are not a brand searching for a story. You have Michael Jordan. You have the Swoosh. You have over 20 consecutive years of dividend growth. You have the world’s biggest sporting event happening in your home country right now.

Yes, the stock chart looks ugly. Yes, the margins are under pressure. Yes, the doubters are loud.

But this is not the moment to play cautious.

This is the moment to remind everyone — investors, consumers, and competitors alike — exactly who built this industry. Stop managing the decline. Start chasing the comeback.

You already have the slogan.

Just Do It.