It’s not the most exciting idea to discuss under most circumstances but Boeing (NYSE: BA) could be an intriguing idea for aggressive debit-side options traders. Basically, the idea is that when BA stock is conditioned for a specific circumstance, there may be a higher probability of performance relative to a random baseline. What’s more, this signal is flashing right now.

To be upfront, I’m not going to waste my time talking about the fundamentals undergirding Boeing stock. The harsh reality is that most financial publications specialize in narrative linear extrapolation using information that is already a matter of public record. As such, you’re not likely to gain an edge from what is nothing more than listening to downstream opinions.

Let’s be brutally honest: in market microstructure terms, by the time a retail newsletter writer notes that a company has a “great brand,” “growing margins,” or a “challenging macroeconomic environment,” that information has already been processed by institutional algorithms, risk-parity models and professional market makers.

Further, it’s incredibly difficult to declare that the market made a mistake in assigning a value on the target security. For example, BA stock is down a little more than 1% on a year-to-date basis. In trailing-month terms, the equity has slipped more than 4%. Bullish analysts might use language to suggest that the selloff is overdone.

However, such arbitration raises the obvious question: how does the analyst know?

Generally speaking, we all agree that the share price of a company represents all publicly available information at that time. So, it’s quite a stretch to assume that some random writer on the internet found a mispricing that every other professional player and institution missed. Unless there’s evidence presented of a mispricing, it’s safe to say such language is simply an example of narrative economics.

For options traders, we need a much more quantitative framework and that’s where an inductive model may be helpful.

No One Knows the True Value of BA Stock

If you really want to know the fundamental argument for BA stock, it’s that the competing Airbus (OTCMKTS: EADSY) A320neo family of jetliners are essentially sold out well into the 2030s. Cynically, if an airline wants to expand its fleet or replace aging jets this decade, it can’t switch to Airbus — the wait times are too long.

Another factor to consider is the de-risked revenue backlog. Boeing sits on a commercial aircraft order backlog exceeding $500 billion (firm orders for thousands of aircraft stretching out over the next decade). Basically, this circumstance provides rare top-line visibility as the demand profile is guaranteed. Some finpubs are using this datapoint to suggest that BA stock is undervalued.

My problem, as I alluded to earlier, is that this backlog — along with other compelling factors supporting Boeing stock — is almost certainly baked into the share price. Therefore, when analysts declare that BA is undervalued, what they’re really saying is that the market somehow hasn’t fully priced in the good news.

I’m sorry but it makes me as a reader ask the glaringly obvious follow-up: what percentage of the good news is not baked into BA stock? 10% 20% What? It’s not an answerable question because — news flash — in order to declare an asset as “undervalued” with absolute certainty, you must first reference an objective, immutable “true” value.

Without that immutable reference, claims of undervaluation are merely supported by trust-me-bro logic.

Using Induction to Trade Boeing Stock

Rather than opine my way toward a conclusion, the more rational solution is to condition the performance of Boeing stock based on measurable signals. If the conditional data outperforms the random baseline, we potentially have an incentive to trade the security. If not, then there’s no point.

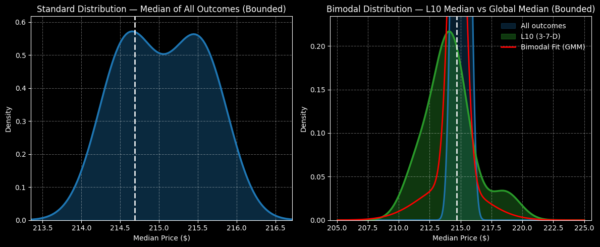

Using data going back to January 2019, a 10-week long position initiated at random for BA stock (assuming a starting price of $214.69) would likely generate a forward distribution landing between $213.50 and $216.50. Further, peak probability density would likely average around $215, thus indicating a modest upward bias.

More importantly, these stats represent our random baseline performance. If a trading signal can’t yield results superior to what we can generate randomly, then it’s not an ideal time to trade.

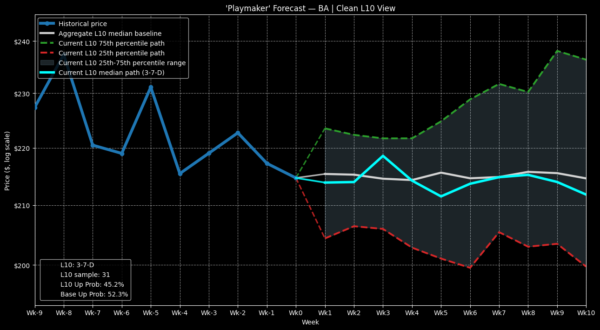

Currently, BA stock is suffering a bearish cycle. In the last 10 weeks, Boeing printed only three up weeks, leading to an overall downward slope across the period. Conditioned for this specific quantitative sequence, the expected forward 10-week distribution is rather poor, clocking in between $207.50 and $221. While the right tail extends further outward, peak probability density of this 3-7-D sequence lands shy of $215, indicating a slightly negative bias.

Based on the data, we wouldn’t want to hold BA stock for a 10-week period following the flashing of the 3-7-D signal. However, when looking at the inductive data on a week-by-week basis, we note that BA stock tends to pop upward in the third week.

If you believe that the same trend will follow after the flashing of the current 3-7-D signal, aggressive speculators may want to consider the 217.50/220 bull call spread expiring July 17. If Boeing stock follows previously recognized patterns, it has a legitimate possibility of reaching the $220 strike at expiration.

Of course, the July 17 expiration represents a near-term target, which doesn’t provide BA stock with much time to trigger the necessary strike. However, because the security tends to be negatively choppy following the third week of the signal flashing, we don’t want to expose ourselves any longer than necessary — otherwise, a profitable trade can quickly become unprofitable.

A Reality Check on Induction

Inductive models rely on pattern recognition but this practice is prone to false expectations, particularly the black swan risk. In other words, just because you see a thousand white swans doesn’t mean all swans are white. Once a black swan appears, the entire presupposition evaporates.

So it is with any inductive model. Just because BA stock tends to pop higher following the third week of the 3-7-D signal flashing doesn’t mean it will do so this time around. But then the question becomes, why bother using induction?

The answer is that I honestly lack any other method that is intellectually satisfying. As discussed earlier, all fundamentally important news has likely been baked into Boeing stock so reiterating this data doesn’t provide any edge. On the technical front, drawing a bunch of support and resistance lines doesn’t automatically grant legitimacy.

At least with the inductive model, we’re attempting to identify patterns based on real quantitative data. It’s not a perfect methodology but it’s arguably the most rational within a non-determinative environment.