Upstream energy giant ConocoPhillips (NYSE: COP) may be down sharply in recent sessions, a victim of an aggressive beta compression from a collapsing crude tape. However, COP stock could elicit a quick scalp for intrepid debit-side speculators. Primarily, the reason for my near-term bullishness is data extracted from a higher-order Markov chain, also known as non-parametric conditional sequence simulation (or path-dependent conditioning).

Standard Financial Analysis is Practically Worthless

Before I get into why I exclusively deal with Markov frameworks, it’s important to understand the severe limitations of standard financial analysis. When a security like COP stock loses 10% of equity value in the trailing month, one of the common, forward-looking assumptions is that the market selloff has “gone too far” or that “the market hasn’t fully priced in the countervailing good news.”

As the reader, your immediate question should be the obvious one: what percentage or portion of the positive catalyst has (or has not) been baked in? And an even more basic question: how does the author know that?

If you look at the financial publication space, you will find an endless library of articles claiming that such-and-such stock is undervalued. However, making such a pronouncement at face value assumes that there is an objective true value that Bob from Arkansas deciphered that no one else — including the biggest institutional players and hedge funds — has found.

I find that to be a remarkable proposition. As popularized by astronomer Carl Sagan, extraordinary claims require extraordinary evidence.

Plus, there’s another big problem with the traditional analysis content mill, which is that the supposed edge that the authors provide their readers is entirely downstream from the events they reference. In the case of COP stock, it’s easy to say that the energy giant is a buy because of the Marathon Oil integration and synergy capture, peer-leading shareholder returns and free cash flow visibility and enhanced capital efficiency and technology spudding.

I think you can spot my concern: this is all public data that has already been disseminated and digested from top to bottom. So, someone would have to explain to me how consuming information at the bottom somehow gives me alpha, which exclusively resides at the top.

Since I refuse to go down the path of deliberate cognitive dissonance, I’m going to present a more defensible proposition and that is this: given a specific bearish condition, the typical pathway of COP stock results in an above-average performance profile over the next five weeks.

Options Data for ConocoPhillips Stock? It’s a Waste of Time.

Usually, I would provide an analysis of unusual options activity or volatility skew for COP stock. I’m here to tell you that these datapoints are completely worthless and that you shouldn’t waste your time (or money) on chasing these data streams.

Let’s think about this matter logically. No one knows with absolute certainty where a stock will go next, whether that’s tomorrow or a decade from now. Given this limitation, how is it possible that the future can be extracted by the derivative of the unknown? If the unknown is unknown, why would a derivative product of the unknown make it known?

Let’s also think about unusual options activity via a critical lens. If there were 50,000 call options bought on COP stock, that doesn’t necessarily mean the market is net bullish. First, someone else is selling those calls, meaning that option transactions don’t just materialize in the ether. Second, by the time big call volumes hit the order books, the market maker has made critical adjustments to stay delta neutral.

Subsequently, those adjustments enhance the implied volatility of the underlying strike price. Invariably, then, if you traded COP stock based on its unusual options activity, you would be buying exposure at peak volatility premiums.

Options data streams are certainly sexy and you feel smart pointing at them and nodding your head. Functionally, though, you’re looking at the telemetry of an airplane that landed an hour ago.

Asking the Right Question

A legitimate analysis of a non-determinative system like the equities market begins with asking the right question. For me, the right question for COP stock is this: given a specific time period, what kind of performance may I expect if I were to just buy shares randomly?

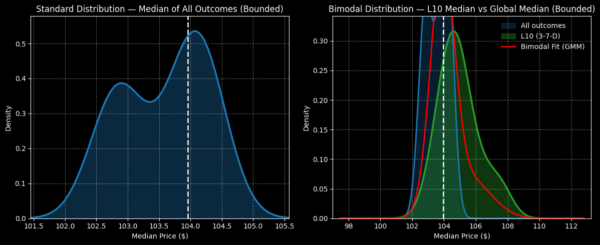

For example, based on data going back to January 2019, a 10-week long position in COP stock would be expected to generate a forward distribution between $101.50 and $105.50 (assuming a starting price of $103.96, Tuesday’s close). Given the shape of the probability mass, you’d be looking at a neutral-to-slightly-bearish bias.

In other words, if you bought COP stock over a 10-week period, it’s basically 50/50 whether you would be profitable or not. So, if you were trading COP conditioned on a specific signal, that signal would have to generate a performance better than 50/50 to be worthwhile.

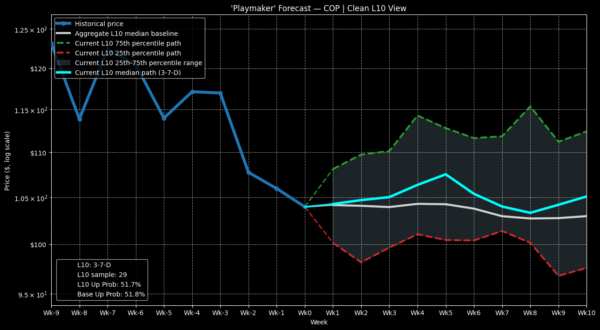

The next question is what’s the signal? I noticed that in the last 10 weeks, COP stock has printed only three up weeks, leading to an overall downward slope. Based on this 3-7-D sequence, the expected 10-week forward distribution would be between $101 and $110, which is noticeably better than the aforementioned random benchmark.

However, the improvement in expected performance isn’t linear. Under the 3-7-D signal, COP tends to rise over the next five weeks before mean-reverting downward. As such, if you accept the inductive framework that this time will be like the other times, a near-expiry bull call spread could be lucrative.

Identifying a Specific Idea

At the most aggressive, I would consider the 105/109 bull call spread expiring July 31. While the $109 strike is on the very edge of the expected distribution, the breakeven price of $107.41 offers a realistic safety buffer. Based on the expected median pathway following the 3-7-D signal, COP stock should be able to hit this target.

Now, the concept of the higher-order Markov chain (where the condition of one state yields a certain probability of transitioning to another state) is hardly foolproof. In fact, because there is no necessary reason why the 3-7-D signal must produce an above-average performance, traders can absolutely get blown up following observed patterns.

Keep in mind that this is a core criticism of all pattern recognition. Just because something happens a hundred times doesn’t necessarily mean that in the 101st time the same thing will also happen. It’s very possible that you can get an outlier, which would destroy the presupposition.

Still, without an inductive framework, there might not be a quantitative mechanism in analyzing public securities. Arguably, as imperfect as Markov chains may be, it’s the best solution we have.