Don’t get me wrong. With the Iranian navy attacking a container ship in the Strait of Hormuz and later announcing that it would close the critical waterway, the spotlight has once again shined brightly on big oil giants like Exxon Mobil (NYSE: XOM) and Chevron (NYSE: CVX). There’s nothing wrong with targeting these securities, especially for longer-term strategies. But for those who are seeking a quick scalp, more love should be directed toward Petrobras (NYSE: PBR).

A Brazilian majority state-owned multinational corporation, Petrobras has suffered a downward slide between the end of April and the beginning of July. However, with the renewed hostilities in Iran, circumstances have cynically moved positively for PBR stock. Over the past five sessions, for example, the security has gained more than 7% of value.

To be fair, the afterhours session on Friday has demonstrated a sideways consolidation. However, with the latest geopolitical spark that was reported on Saturday evening by the New York Times, it’s quite likely that PBR stock and the broader fossil-fuel energy market will rise.

Of course, that’s an obvious inference as a renewed conflict would again impose an inflationary crisis on the global economy, not to mention the catastrophic energy supply chain disruption. Because there’s so much at stake, there’s a non-zero probability that the Trump administration will back down. From just a political angle, the war is deeply unpopular. Plus, it wouldn’t be the first time the White House walked back its previously tough stance.

With that in mind, I’m looking for a near-expiry debit-based options trade. By this, I believe that an argument could be made for a directional trade. Under this framework, I want to pay a debit (start from a cash outflow position) to bet on a particular outcome materializing. Essentially, a debit spread on PBR stock is a low-probability, high-reward wager.

However, it’s more than possible that the way the “low probability” is measured by the market is flawed, opening a door to astute retail traders.

How the World Cup Provides a Lesson on Petrobras Stock

For sports fans everywhere, this year is particularly magical because of the World Cup. Even casual observers have tuned into the soccer tournament as they cheer on the globe’s best players. But what’s fascinating about the beautiful game is how the structure changes as soon as one team scores.

Typically, following the initial kickoff, both teams are cagey — feeling each other out while making sure not to make an early mistake. But as the game drags on and a team eventually makes a breakthrough, the nature of the competition changes. Suddenly, the team with the lead has an incentive to be more defensive-minded, while the team that was scored on must chase the game.

At half-time, each manager could make strategic and personnel changes — all in response to one goal. Now, the question for PBR stock or any other publicly traded security is this: if a soccer team changes how it operates based on shifting conditions in the game, why would the equities market be any different?

Here’s a clear, quantitative example. In the last 10 weeks, PBR stock printed only three up weeks, leading to a downward slope. Before I get into the forward 10-week distribution conditioned for this 3-7-D sequence, ask yourself this: would Petrobras stock respond differently if it had printed only three down weeks, thereby leading to an upward slope?

My theory is yes, the market would almost certainly act differently. Why? Because nowadays, the dominant forces in the equities sector use algorithmic or rules-based trading. When the algos of advanced hedge funds notice that PBR stock flashes a 3-7-D sequence, it may interpret that as a temporary discounted opportunity. Even better, the data puts inductive weight on the theory.

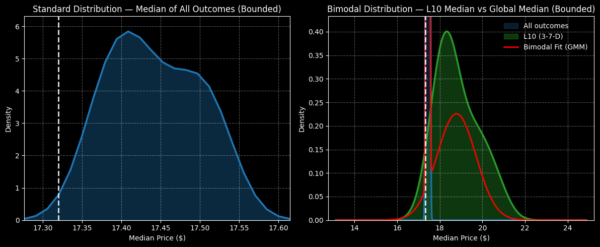

Conditioned for the 3-7-D sequence (which has flashed 24 times on a rolling basis since January 2019), the expected 10-week forward distribution of PBR stock would likely stand between $16 and $22, with probability density peaking around $18.20. That’s assuming a starting price of $17.32, Friday’s close.

Why is this observation significant? Because as a random baseline, the expected forward distribution of PBR stock would be between $17.25 and $17.60, with probability density peaking near $17.41. On average across the spectrum, you’re looking at a 4.54% positive variance.

Playing the Inductive Card Shrewdly for Petrobras Stock

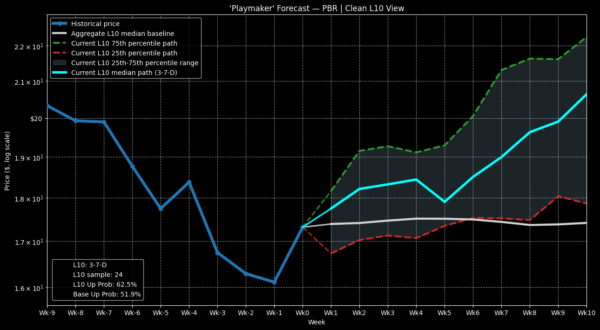

Although the forward distribution of Petrobras stock under 3-7-D conditions statistically has a better expected performance outcome than the random baseline, the trajectory may not be linear. From an inductive viewpoint, PBR has a tendency of rising through the first four weeks before taking a conspicuous dip on week 5.

Obviously, there’s no guarantee of the uniformity of nature, meaning that anything could happen this time around. However, if we were to play the numbers, the 17.50/18 bull call spread expiring July 31 could be interesting. Over the next three weeks, PBR stock would be expected to rise through the $18 level, which should trigger the second-leg strike. Doing so at expiration would result in a 150% maximum payout.

What’s really eye-catching here is the net debit, which is only $20 per spread. It’s a tantalizing opportunity but the reason is that the market only assigns a probability of 38% that PBR stock will rise to $17.70, the breakeven point for the above spread.

While 38% sounds dangerously low, this figure is calculated largely by the distance (in standard deviations) the spot price is from the target threshold, assuming a risk-neutral, log-normal distribution. However, as I just explained with the World Cup example, a distribution of outcomes is likely to change based on shifting conditions.

In this case, we shouldn’t calculate the probability of PBR stock assuming risk neutrality. Instead, we must calculate it based on its current sentiment state, which is negative. Observationally, because of the extended negativity, there’s a greater chance of positive mean reversion.

Fundamentally, I dispute the market’s low probability of profit (reaching breakeven). Indeed, the odds that Petrobras stock rises above $17.32 by the end of week 3 is 70.8% (or 17 occurrences over 24 times). I wouldn’t be surprised, then, if the chance of PBR hitting $17.70 is between 58% to 60%, not 38%.