General Mills (NYSE: GIS) isn’t a stock you trade. It’s a stock you own. That distinction matters more than ever after the company’s fiscal 2026 fourth-quarter report, released July 1. Shares sit near their 2026 lows around $36, well below the stock’s 200-day moving average of roughly $42. However, the dividend yields close to 6.7% at current prices. For income investors willing to look past a rough year, that combination of depressed price and dependable payout is worth a second look.

A yield that high can be a warning sign. Elevated yields often precede a dividend cut, especially in consumer staples names fighting volume declines. But General Mills’ payout looks safer than the yield alone suggests. Coverage remains intact, and management has laid out a multi-year cost-cutting plan designed to protect it. The bull case here isn’t about a near-term turnaround. It’s about getting paid to wait for one.

The Numbers Behind the Story

Fiscal Q4 organic net sales came in flat, an improvement from the 2% organic decline for the full fiscal year. Adjusted operating profit jumped 13% in the quarter, and adjusted diluted EPS rose 27%. Both numbers benefited from an extra week in the reporting period and favorable trade expense timing. Strip those tailwinds away, and the underlying trend looks less impressive. Full-year adjusted operating profit fell 16%, matching the decline in adjusted diluted EPS to $3.55.

Margins make the story even uglier. Adjusted gross margin slipped to 33.5% from 34.5% a year ago, largely on higher input costs. Adjusted operating profit margin fell further, from 17.2% to 15.3%. Management blamed a mix of cost inflation, softer volumes, and heavier marketing spending, particularly in the North America Pet segment.

Pet is worth flagging on its own. It had been a growth engine in recent quarters, but organic net sales there declined 3% in both the fourth quarter and the full year, driven by retailer inventory changes. That’s a shift investors should watch closely in the coming quarters.

Guidance Sets a Cautious Bar

Fiscal 2027 guidance calls for organic net sales of -1.5% to +0.5%, adjusted operating profit down 8% to 13%, and adjusted diluted EPS of $3 to $3.20. That means earnings are expected to decline again next year, even after this year’s drop. Management attributes roughly nine points of the operating profit headwind to lapping the extra week, normalizing incentive compensation, and the impact of the completed U.S. yogurt divestiture.

Offsetting that, General Mills is targeting $750 million in cost savings for fiscal 2027, part of a broader plan to reach $3 billion in cumulative savings by fiscal 2030. Free cash flow conversion is guided near 95%, though fiscal 2026 operating cash flow actually declined to $2.166 billion from $2.918 billion the year before.

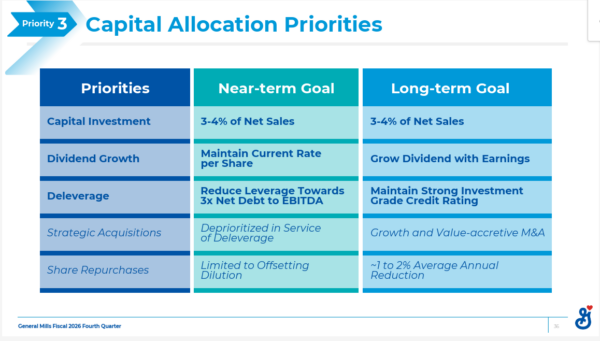

The Buyback and Dividend Picture

General Mills repurchased $500 million of stock and paid $1.315 billion in dividends during fiscal 2026. That combination reduces the share count over time, which helps offset the cost of future dividend increases. But investors shouldn’t expect an aggressive near-term buyback push. Management’s own capital allocation framework lists share repurchases as “limited to offsetting dilution” in the near term, with the more meaningful 1% to 2% average annual share reduction reserved as a longer-term goal.

Deleveraging toward a 3x net-debt-to-EBITDA target currently takes priority, and even strategic acquisitions have been deprioritized in service of that goal. The dividend itself is being held at its current per-share rate for now, not grown, while the balance sheet gets repaired.

Why the Valuation Still Works

At roughly 11 to 12 times fiscal 2027 guided earnings, General Mills trades well below its own historical average and below the broader consumer staples sector. That’s not a stock that’s cheap simply because it trades under $50 a share. It’s genuinely inexpensive relative to its own cash-generating capacity, assuming the cost-savings program delivers as promised.

The bear case is straightforward. Category growth across packaged food remains slow. Consumers are trading down to private label, and General Mills has explicitly cited weight-loss trends and shifting consumer health perceptions as ongoing risk factors in its own filings. If that behavioral shift proves structural rather than cyclical, volume pressure could persist longer than management expects.

Technically, there are early signs of stabilization. The stock’s MACD has turned positive for the first time since early 2026, suggesting selling pressure may be easing even though the price remains below the long-term moving average.

Consumer Psychology Will Ultimately Decide GIS Stock’s Next Chapter

If shoppers have permanently decided that store brands match General Mills’ quality, that’s a real long-term problem. However, if this is simply a cyclical squeeze from inflation and gas prices, the setup here is straightforward: collect a well-covered dividend, let buybacks work in the background, and wait for volumes to normalize.

Until that question is answered, General Mills remains a name to own patiently rather than trade actively.