Exxon Mobil (NYSE: XOM) easily ranks among the most difficult investments to assess thanks to the shifting tides of the Iran war. However, with cooler heads finally prevailing in the conflict, a serious question mark hanging over XOM stock has been significantly mitigated. Assuming that tensions continue to unwind in somewhat of a transparent manner, the integrated oil market could be intriguing from a structural or mechanical perspective.

By that, I mean that I don’t want to focus on the fundamentals impacting XOM stock. Such a statement might sound sacrilegious but there are three incontrovertible conclusions that any intellectually honest analyst reaches:

- The market has digested all possible catalysts.

- In case of partial digestion, you are never sure what the market has or has not digested.

- Even if you are sure, the market might not care.

Invariably, the financial publication industry thrives on insights and correlations found in various companies’ quarterly statements and other material corporate disclosures. But the problem here is that the era of analysts in nice suits pouring over corporate literature has mostly faded. Today, trading decisions occur in nanoseconds thanks to high-frequency algorithms.

Let’s also be real here: it’s highly unlikely that random independent contributors (like yours truly) are able to extract profound insights that Wall Street completely missed. As smart as we might think we are, we are always operating downstream of the information flow. Therefore, whatever I have to say about XOM stock has long been integrated into the share price.

Even if that were not the case, there’s no telling what the Street has or has not accounted for. Because XOM stock lost 10% in the trailing month, you’ll almost surely come across analysts that declare that the selloff is overdone. But that statement assumes knowledge of a true intrinsic value of XOM stock that thousands upon thousands of professional investors missed — but somehow Bob from Arkansas got right.

Forgive me but I find that premise to be implausible. And even if valid, the market can ignore your precious insights far longer than you can stay solvent. That’s the cruel reality of a non-determinative system.

A Spotlight on the Market Mechanics of XOM Stock

Since analyzing the fundamentals will likely be a fool’s errand for a flagship equity like Exxon Mobil stock, arguably the best approach (i.e. the least crappiest) is to focus on XOM’s market mechanics. In other words, I don’t think the oil company’s PE ratio is the fulcrum for where shares will head next. Rather, we’re left with observing how XOM responds to certain triggers.

One of those triggers (in my opinion) is the mean-reversion theory. As stated earlier, XOM stock has lost 10% in the trailing month. Since the end of March, the security is down roughly 20%. Yes, as a vibe, most people might say that Exxon Mobil’s selloff is overdone. Thanks to modern technology, though, we can measure these assumptions and build a probabilistic, forward-looking framework.

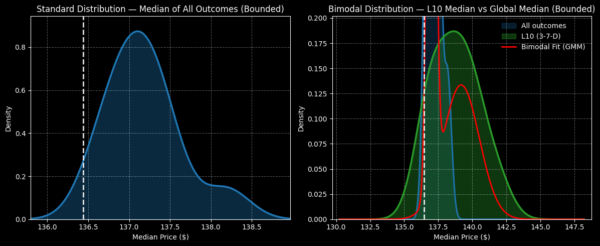

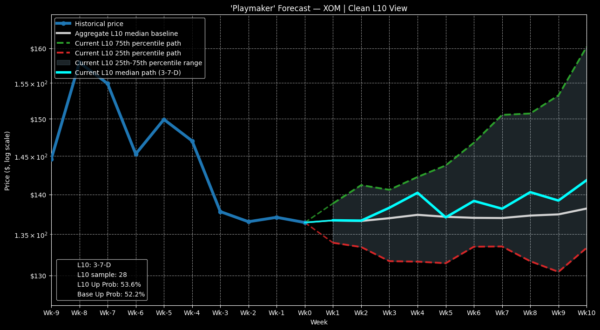

From a quantitative perspective, Exxon Mobil stock has printed only three up weeks in the last 10 weeks, leading to an overall downward slope. Conditioned for this 3-7-D sequence (using a dataset going back to January 2019), bullish traders may expect a forward 10-week distribution landing between $133 and $145, with probability density peaking at around $138.50 (assuming a starting price of $136.44, Monday’s close).

Why is this distribution of likely outcomes significant? Because under random conditions, buying XOM stock (at the same price above) and holding the security for 10 weeks leads to a forward distribution between $136 and $139, with probability density peaking at $137.20. Because the risk-reward curve expands net bullishly under 3-7-D conditions, there’s a theoretical incentive to buy XOM stock right now for a (short-term) swing trade.

Of course, the question comes up about why this analysis should matter? The answer is that because all catalysts (both positive and negative) have been priced into the XOM stock price, there’s no edge that reading yesterday’s newspaper can provide. As such, the only real edge that is relevant is the mechanical one.

I’m demonstrating here that under a specific bearish state (i.e. the 3-7-D sequence), the chance of a positive mean reversion occurring is elevated — and that the median expected performance often results in a net return that is typically greater than the random baseline.

Going for a Specific Trade

Although the expected distribution for the above signal is tempting for speculators, the projected upside is not expected to follow an orderly, linear trajectory. From prior observations, the fourth week features a sizable pop before somewhat fading. As such, I’m interested in the 138/141 bull call spread expiring July 31.

If we take the inductive logic above at face value, the $141 price target is a realistic objective. If XOM stock manages to rise through this second-leg strike at expiration, the maximum payout stands at over 105%. Further, the breakeven price for this spread comes in at $139.46, providing some margin for safety.

What makes this trade a contrarian proposition is that the Black-Scholes model pegs the probability of XOM stock breaking even at only 38.3%. However, this calculation largely stems from how many standard deviations the target threshold is away from spot, assuming a log-normal distribution of outcomes. It’s this latter point which I have a significant disagreement with.

My theory is that stocks do not necessarily follow a log-normal, risk-neutral distribution. Rather, when risk is heavily concentrated — as it is with Exxon Mobil stock thanks to its recent underperformance — there’s a greater reactive risk of the security bouncing higher due to mean reversion.

The key distinction with my analysis compared to the rest of the finpub industry is that I’m not just saying XOM stock will rise higher due to mean reversion. Instead, I’m using past empirical data conditioned for a specific bearish sequence to calculate forward tendencies.

Of course, the main risk with any inductive model is that the uniformity of nature cannot be assumed. Basically, I’m hoping this time will be the same but it could also be different. I’m just relying on the mechanical tendencies of the market to help steer me correctly more times than incorrectly.

If you accept this premise, Exxon Mobil stock could be very intriguing over the next few weeks.