It’s an understandable thesis. With Disney (NYSE: DIS) suffering a disappointing performance this year, shedding more than 14% of market value since the January opener, it’s reasonable to assume that mean reversion could send DIS stock higher. After all, the equities market is a reactive system, responding in a dynamic manner to acute pressure.

In fact, the concept that public securities respond differently to specific triggers is the basic foundation of my higher-order Markov simulations. Under standard trading frameworks like Black-Scholes, risk is defined as the distance (in terms of standard deviations) between the spot price of an asset and the target threshold, assuming a log-normal distribution.

However, I have consistently refuted the idea that market distributions can be assumed to be log-normal. Even if they were, I especially find it erroneous that log-normal functions would apply irrespective of the security’s sentiment state, whether bullish, bearish or consolidatory. Despite this, with DIS stock suffering a prolonged downturn — such as a 52-week loss of nearly 20% — a common conclusion is that the selloff may be overdone.

We’re talking about Disney. Yes, the company has suffered some missteps, including embroiling itself in political and ideological controversies. Nevertheless, it’s still a media and entertainment powerhouse, commanding incredibly desirous brands and content franchises. That’s got to be worth something; hence, the belief that DIS stock can rebound higher.

While the theory makes sense, mean reversion can’t be assumed wholesale. It’s one of the criticisms/concerns that I have about how technical analysis is commonly practiced in the financial publication ecosystem. Just because it’s asserted that, say, the cup-and-handle formation probabilistically leads to a bullish outcome doesn’t mean the argument is valid.

You have to check for the security at hand. It’s very possible that certain names may respond differently to established technical patterns. So it is with DIS stock. Let’s not assume that it’s going to automatically mean revert because it’s suffering a bearish cycle.

Instead, we should verify the implications from the data.

Laying Out the Conditional Inference of DIS Stock

Now, I don’t think it’s a controversial point to discuss the psychological market dynamics surrounding a contrarian bullish position in Disney stock. Primarily, the observation is that securities suffering a bearish cycle practically never fall in a smooth, linear fashion. Instead, even the most pronounced downturns are met with reactionary upswings.

What’s the reason for these countermoves? Basically, human market participants do not have infinite risk tolerance. During an extended downturn, the weak hands holding a security may be systematically shaken out through trailing stop-losses, margin call liquidations and pure psychological capitulation. When that happens, the bears suffer an exhaustive phase, opening the door for the contrarian bulls to shoot the security above weakened resistance levels.

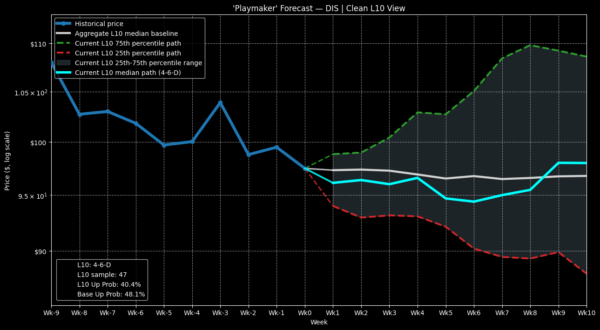

As sensible as this assumption is, the data at this point doesn’t support a contrarian position in DIS stock. In the last 10 weeks, Disney printed four up weeks, leading to a downward slope across the period. Since January 2019, this 4-6-D sequence has materialized 47 times on a rolling basis.

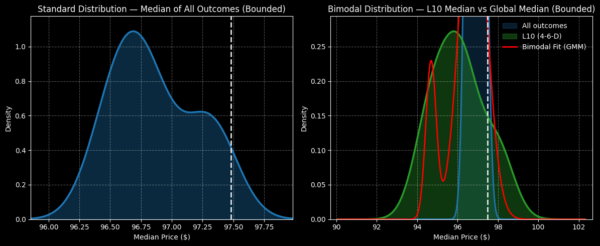

If this bearish sequence consistently led to positive mean reversion, we would expect the median distribution of outcomes to beat the random baseline (that is, the net return of buying DIS stock randomly). Unfortunately, that’s not what the data shows. Conditioned for the aforementioned signal, Disney’s expected forward 10-week distribution would land between $92 and $100, with probability density peaking just shy of $96.

What’s the problem with this range? It assumes a starting price of $97.48, Tuesday’s close. If over the next 10 weeks, the median representative price across the spectrum is $96, you’re talking about a negative exceedance ratio.

Technically speaking, you’re actually better off buying DIS stock randomly, which since January 2019 has not been an effective solution. If you just bought Disney stock with no regard as to waiting for a specific signal, your forward 10-week distribution would likely land between $96 and $98, with probability density peaking at $96.70.

In both cases, the frequentist argument would likely see your head underwater.

A Nuance to Consider

To be honest, the bullish contrarian case for Disney stock isn’t completely dead. Under the 4-6-D sequence, the 75th percentile pathway shows potential for DIS hitting $110 (around week 8 of the forward 10-week distribution). Further, the 25th percentile pathway is asymmetrically mitigated on a relative basis, dropping to around $89 at week 8.

Of course, the problem is that neither the 75th nor 25th percentile pathways are likely; they merely represent what could happen during outlier cycles. That’s not to discourage you from considering the bullish case, per se. However, you really need to consider the frequency risk.

Basically, if you ran this trade across a hundred parallel universes, you would likely lose at least 60 times. Obviously, that’s not an edge for the bulls. However, it could be an idea for near-term bearish speculators to consider.

According to an inductive calculation of DIS stock under 4-6-D conditions, the median price of shares has demonstrated a tendency of sagging between weeks 5 and 7. If the pattern holds true this time around, we may expect DIS to linger at around $95 before marching higher in week 8 and beyond.

Should you believe in the pattern recognition, the empirically sensible idea is to consider the 100/95 bear put spread expiring Aug. 21. Should DIS stock fall through the $95 strike at expiration, the maximum payout stands at over 85%. The net debit per spread comes out to $270, with the breakeven price clocking in at $97.30.

What makes this trade tick for me is that the market is assigning a probability of only 49.4% that Disney stock will fall to the breakeven price. Again, this probability assumes a log-normal, risk-neutral distribution, which I disagree with. Instead, I believe acute pressures cause acute responses. While it’s incredibly difficult to provide a hard answer, I’d estimate that the “real” probability is between 55% to 60%.

Frankly, I don’t think the mispricing is wide enough to justify much excitement. However, I do believe that in the near term, the bears may have more influence on DIS stock than the bulls.