Although one of the most celebrated names in artificial intelligence, Oracle (NYSE: ORCL) is now facing a severe reality check. Since the start of the year, ORCL stock is down 28%, largely a byproduct of recent underperformance. Specifically, in the past month, the security has found itself down nearly 34%, raising serious questions for investors.

On surface level, it’s not too difficult to see why Wall Street has been freaking out. Fundamentally, the immediate structural threat to Oracle’s valuation is the sheer cash consumption required to build Oracle Cloud Infrastructure (OCI). For fiscal year 2026, the company’s capital expenditures skyrocketed to $55.7 billion (compared to $21.2 billion a year earlier).

More distressingly, management shocked the market by guiding fiscal 2027 capex even higher — to an astronomical $90 billion to $95 billion. And because capital investment has heavily outpaced operating cash generation, Oracle reported a massive negative free cash flow of $23.7 billion for FY2026. Adding to the woes, FCF is not expected to turn positive until 2029.

Essentially, skeptics are arguing that Oracle is trading a historically high-margin, predictable software business for a highly asset-heavy, capital-intensive utility model. As such, the discount rate of ORCL stock — which isn’t a single number but a highly complex, multi-layered compound of variables that are constantly shifting gears in real time — had to endure a massive shift to reflect the new risk paradigm.

What that means is exactly what you’re seeing: a sharp technical collapse of ORCL stock. But now the question is, has the market potentially overreacted to the bad news?

As mentioned before in prior articles, I’m not too big on the idea of market overreaction — the price is the price. Put differently, the current level of Oracle stock represents the digestion of all publicly available data tied to the underlying organization. That said, the news isn’t exclusively terrible for ORCL.

Don’t Fall for Poorly Constructed Arguments for ORCL Stock

If you quickly peruse the financial publication ecosystem, you’ll notice that many articles favor the bullish case for Oracle stock, primarily under the thesis that the security is discounted relative to the fundamentals. However, I believe this reasoning ignores the fundamentals of risk management.

Sure, ORCL stock currently trades at 24x trailing-year earnings. Yes, just a few months ago, it traded at over 40x and about this time last year, it exchanged hands at 52x. That doesn’t automatically make Oracle a discount. Let’s think about this logically: if investing/trading were that easy, wouldn’t you just use a screener to identify “discounted” P/E ratios?

Further, who is to say that the market is wrong about ORCL stock and its current valuation? Bob from Arkansas? Again, let’s think about this logically. If value could be unlocked by simply looking at companies that lost value, what would the point be of doing any analysis on any company? What would be the point of reading any article? You would simply look for red ink and be done with it.

From a financial perspective, the bulls do have a massive card to play: the company’s Remaining Performance Obligations (RPO), which hit an astronomical $638 billion at the close of its FY2026 fourth-quarter results in June. This figure represents a 363% year-over-year increase, fueled by adding $85 billion in new contract bookings in Q4 alone.

Basically, the bulls are arguing that the shift in Oracle’s business isn’t something to be overly concerned about; we’re talking about demand that isn’t theoretical but is contractually locked in. Moreover, while the bears often treat Oracle’s legacy database software as a melting ice cube, it’s experiencing a massive second life via strategic partnerships. It’s no surprise, then, why so many are keen on the contrarian case of ORCL stock.

Nevertheless, the positives don’t make for clean green light for Oracle stock. The reason? There’s no evidence to suggest that the backlog RPO and other positive catalysts have not already been reflected in the rerating of ORCL. Plus, it’s not that the Street doesn’t see the RPO. Rather, investors are largely worried about the nature of how that backlog must be serviced.

An Inductive Model Doesn’t Signal Much Variance

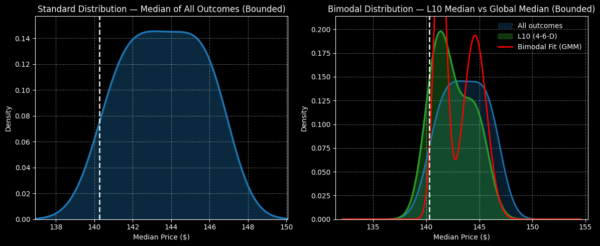

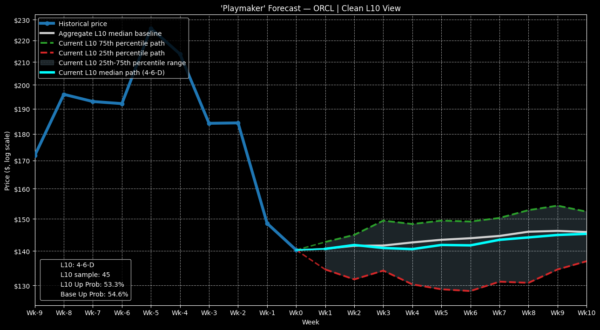

Ultimately, we can argue about the fundamentals (and what is and isn’t priced) but it truly comes down to how the market will respond to ORCL stock. If we were to buy shares randomly and hold them for a 10-week period, a calculation based on a dataset going back to January 2019 reveals an expected median distribution between $137 and $150 (assuming a starting price of $140.27).

With probability density peaking at just south of $144, ORCL stock enjoys an upward bias. This is our random baseline and therefore, trading signal must beat this benchmark.

Right now, the argument is that because Oracle stock has suffered a sharp bearish cycle, it’s more likely to see a positive mean reversion — but is that really so? In the past 10 weeks, ORCL printed four up weeks, leading to a downward slope. Conditioned for this 4-6-D sequence, we would expect the forward 10-week distribution to land between $137 and $148, with probability density peaking at around $142.

Obviously, that’s a poorer performance than the random baseline, which means that from a bullish perspective, there’s no incentive to trade ORCL stock at this hour.

Even when looking at a week-by-week basis, the expected median performance of ORCL following the 4-6-D signal flashing is only better than the random baseline for one week (in the second week following the signal). Otherwise, from an observational perspective, betting on Oracle randomly typically provides better results.

To be fair, the philosophical criticism of any inductive model is that the uniformity of nature cannot be assumed. Therefore, just because we see consistent patterns of underperformance associated with the 4-6-D sequence does not necessarily mean that ORCL stock is doomed to underperform here on out.

However, it’s also important to realize that just because an inductive framework is flawed doesn’t necessarily mean that the opposing idea (in this case, that ORCL is a contrarian buying opportunity) is automatically valid.

Mainly, I don’t have evidence that the market is ignoring Oracle’s positives. Combined with the lack of evidence that ORCL mean reverts under the current setup, arguably the more reasonable idea is to wait for a more decisive signal.